ВУЗ: Не указан

Категория: Не указан

Дисциплина: Не указана

Добавлен: 18.10.2024

Просмотров: 255

Скачиваний: 1

Controlling the way companies do business. Controlling what companies sell. Controlling the prices companies set.

Before you listen

Discuss the following with your partner.

Here is a list of arguments against state-run hospitals and arguments against private hospitals.

fij

F Listening Щ)))

Now listen and check your answers.

badly organised

creates a class of poor, unhealthy people

hospitals in bad condition

hospitals will reduce costs to make money

is bad for society in general

long waiting lists for patients

only the rich can afford health care

staff are poorly paid

taxpayers support everyone

|

Against state run hospitals |

Against private hospitals |

|

|

|

P G Speaking

Discuss these questions with your partner.

Do people only work for money? What other motivation is there to work?

Task

Work in groups of three. Each of you will take one of the following roles.

STUDENT A

You believe that the planned economy is best.

STUDENT В

You believe that the free market is best.

STUDENT С

You believe that a mixed economy is best.

Take turns to present arguments to support your ideas for the best economic system.

Remember to include:

why the system is good for the economy

why it is good for society

When each of you has presented his or her argument, have an open discussion.

Write an essay comparing the planned economy with the mixed economy. Discuss the advantages and disadvantages of each economy. Decide which is best in your opinion.

Use these words and phrases to organise your ideas:despite this, nevertheless, consequently, in contrast, similarly

Read texts 1 and 2 again and use these notes to help you. Write four paragraphs.

Discursive essay

PARAGRAPH 1

What is a planned economy?

What is a mixed economy?

Introduce the subject by saying generally there

are these two kinds of economies that have

advantages and disadvantages.

PARAGRAPH 2

Describe a planned economy, explaining its advantages and disadvantages.

PARAGRAPH 3

Describe a mixed economy, explaining its advantages and disadvantages.

PARAGRAPH 4

Conclude by saying which system you think is

best.

Or

Explain why you think neither system is the best.

Write 200-250 words

Pronunciation guide

Commodity koniixbti Shortage '[л:П(1> Hoard li.iid Drawback 'ilr.\b<rk Enterprise Ч'Млрпш Deregulation di:ioi)juloi[n/ Guarantee /q&'ivmti:.

4 * ( T 11 i r (j j -1 * t fron.. m . i г 111 * 23

Revision Vocabulary Units 1 to 4

Complete the crossword. Some letters have been given to help you.

|

M |

|

|

H |

|

|

-M | |

|

||||||||

|

|

|

|

тi |

|

|

|

|

|

|

|

|

|

L | |

||

VI

I)

M

Г I)

ACROSS

This kind of economy is both planned and free market.

The fust k;nd of economy that existed.

The point where demand and supply meet.

This kind of economics simply describes the economy.

A measure of how much demand influences price.

This kind of economics makes recommendations.

This kind oi economics locks at the details of the economy.

DOWN

This kind of economics looks at the whole picture. In this economy, the government decides everything. This falls as prices rise.

In this kind of economy, price is set by supply and demand.

Something that can be measured, like money spent or babies born.

B1 Find six pairs of opposites.

P B2Now write five example sentences using as many words as possible from this exercise.

Complete the text with one word for each gap.The first letter has been given.

The traditional economy is the oldest form of economy. it has existed for thousands of years, although today it has almost disappeared. People in a traditional economy do not own

(l)p They do not earn a

(21 sand thus neither do they pay

(3) tIn fact, there is no money.

They live on the raw (41 mthat the

forest provides them. They don't grow food or

have any organised (5 a with farms

and (6) с growing in fields. Instead,

they (71 gwild fruit and vegetables

or (8) hwild animals. They eat most

of the food they find, and may (9) h

some food for the winter, but they do not sell it. It's

a difficult life. There are often (10, s

of food when there is not enough to eat. When this

happens, the (lit must move on to

another part of the forest.

I benefits ■ consumer ■ drawbacks I drought ■ flood ■ manufacturer I private sector ■ save ■ shortage I spend ■ state sector ■ surplus

)AMirw ' -С, (. 1 ГТП EfCl«n-Ki <? Ю I • О Г V Г Г i Г ; * ' * I-1M I ro 4

Figure

1: Budget Line

Chotoi M«l <

Before you read

г т

WaUfD

€2

лboltW

-» budget -» the price

>

ff A Vocabulary

Choose the correct word or phrase.

If you are m a hurry, it can be difficult to make a decision.

The amount of money you have to spend is your

budget constraint / deciding factor.

The speed limit on this road

is 120 kilometres per hour.

Quality is often the

when people choose something to buy.

Some people how much they

spend every week.

Green isof

yellow and blue.

When you buy something from a shop, you make a

purchase / budget constraint.

When you something is true,

you guess that it is true.

The use or satisfaction you get from something you buy is called

Olive oil is a healthy to butter.

IS Reading 1

Consumer choices

It's a hot summer day. You've been out walking all morning and you're getting thirsty. It's also about hmehtinic, and you're feeling pretty hungry, too. What luck! Here's a kiosk selling snacks. You've got six euros to spend. You can buy bars of chocolate or bottles of water ... or a combination of both. Now you've got another problem: consumer choice.

It you're a two classical economist.however, there's nothing to worry about. Neoclassical economists believe that consumers make rational choices, before a consumer buys something, they think about the cost and the amount ot satisfaction the purchase will give them They then compare the price and satisfaction of possible alternative purchases. In the end. they buy what gives them maximum satisfaction at the lowest cost.

So. what will you buy from the kiosk'r An important deciding factor is the amount you have to spend. Keonomists call this your 1>и<1це1 constraintYour total budget is six euros, bottles of water arc two euros each, chocolate bars are

Mlr m.lui Gli'de tn F f л л о fr U* Г 5 25

one nun each. You could buy three l>ottlcs ot water, or you could buy six chocolate bars. < )r. you could bu\ any combination that adds up to your total budget We can put all ot this information ona budget hue. like the «'tie in tigure 1. The budget line shows what combinations o! go< к Is are possible. Kcouonnsts call these combinations ot'goods hum lies |!ut which is the best bundh r I las depends on something called utility Л'tility is the eeonomists' word tor the satisfaction we get from a purchase. Kach good has its own utility v alue for the consumer The utility of a bundle depends on two things: the utility of the goods in the bundle, and how much of each good is in the bundle Figure 2 on page 25 shows the bundles ol chocolate and water that give the same level of utility. This kind of chart is called an indifference curve. Any point on the curve has the same utility value as any other point. For example, two Kittles of water and two chocolate bars has the same utility as one bottle of water and font chocolate bars.

In tigure 2. we assume that chocolate and water have tin same utility value for the consumer. Hut it water had a higher utility value than chocolate, the curve would be a different shape. Many things can affect the utility of a good. These include the cost of the good, the consumer s income and something called uuimhuil utility

To understand marginal utility, just think about chocolate bars. К very time you consume a bar ot chocolate, tile satisfaction you get from the next bar will be less In other words, you get less utility every time you eat another bar. This decrease in utility is called the marginal utility. The marginal utility is tlu one of an additional item, l or example:

|

liars ot |

Marginal |

Total |

|

chocolate |

I 'tility |

I "tility |

|

0 |

- |

0 |

|

1 |

1(> |

10 |

|

> |

0 |

1') |

|

|

s |

27 |

|

I |

7 |

M |

I'm very simply, budget, price and level of utility will all affect vour choice at the kiosk. The neoclassical theory of consumer choice says that it is possible to calculate demand for products if we know this kind of information. However, not all economists agree!

M I ! . f'C, j. A W \J Eionoc-.ii . * ■»

Now read the text again and answer the questions.

According to neoclassical economists, what do consumers want?

The most satisfaction at the lowest cost. The cheapest product. To spend all their money.

What is budget constraint?

An amount of money you want to save. A combination of money and satisfaction. The total amount of money you have to spend.

What is utility?

How much of a product you get. The satisfaction you get from a product or service.

The cost of a product. What explains marginal utility?

The more satisfaction something gives you. the more you want it.

The more satisfaction something gives you, the less you want it.

The more you have of something, the less satisfaction it gives you What do neoclassical economists behove about consumers?

They make logical decisions.

They always know what they want before they

go shopping.

They don't know what they want.

Before you listen

Not all economists agree with the theory of consumer choice described in the text. Here is a list of reasons why. Complete each sentence with a word from the box.

В С Listening Щ)))

ч

advertising ■ constraints

information ■ mistakes ■ rational

V

Consumers are not always

Consumers often don't have enough

Choices are affected by

Consumers make

Budget may not guide consumers'

choice.

Now listen and check your answers.

Before you read

Discuss this question with your partner.

-* What do you think a company has to spend money on? Make a list ol your ideas.

^ D Vocabulary

Figure

3: Constant return to seal*

A

Variable

Costs

1С)

tone люо .«cm 4ooo як» woo /000 moo9000 10000Production units (e.g. pens)

interest keep track of loan

maintain minus nasty part-time rate relationship

revenue the short term

: I whit I spend by writing

everything down in a notebook

There is a between the quality of a

produci and its cost.

A company's total is all tho money

it receives from sales.

is the next few weeks or months

The long term may be the next years or decades.

Five three is two.

Factories have to then machines to

keep them working properly.

A worker works for only a few

hours a day or a few days per week.

When someoneor something is

they aren't nice at all.

When somebody lends money, they are giving a

The at which something happens is

how fast it occurs.

Variable

Costs

(€)

Figure

4: Dis cconomy of scale

1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 Production units (e.G. Pens)

Costs and supply

('omp.'iiiivN have to spend money in order to make money The money they spend ю manufacture their Jljoods or pro\ ide lilt it sel\ icesare called ei».s/.s. Costs arc important. Any company that doesn't keep track of costs will soon |>e in trouble. And there are many different kinds of costs to keep track of such as_ fiver/ cimtn andvariablt casts

M»f*

I а я Си 3 Ш to С J n Q f- U. I & 27

One type is fixed costs.Fixed costs are costs that don't change. They are costs that the company has to pay each month, for example, or each year. The value of fixed costs will not rise or fall in the short term. Examples include the rent the company pays, the interest they have to pay each month on any loans and the salaries they have to pay lor permanent employees. The good news about fixed costs is that they don't change with increases in production. For example, imagine a company produces 1,000 pens in January and 2,000 pens in February. The rent for the factory remains the same for both months.Variablecosts, however, change (vary) with the size of production. The more pens the company produces, the more these costs increase. Examples of variable costs arc the raw materials needed for production, the cost of electricity and the cost of maintaining machines that are working more. Also, the company may need to get more part-time employees. Their hourly pay is another variable cost. In unit 1 we said that the price of a product or service increases as supply increases. Variable costs are the reason why.

1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 Production units (e.G. Pens)

In a

perfect world, variable costs will increase steadily as production

increases. This is called constant return to

scaleand it is shown in figure 3 on page 27.

However, this is not a perfect world! Sometimes, variable costs rise

at a faster rate than production. This nasty situation, which is

called a

dis-economy of scale,is shown in figure 4 on page

27. On the other hand, companies sometimes get lucky. Variable costs

can rise at a much slower rate than production. This is called an

cconomy of scale,and is shown in figure 5 below.

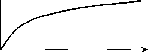

Figure 5: Economy of scale

Variable Costs (€)

Micro

В E Comprehension

Now read the text again and answer these questions in your own words in the space provided below.

What are costs?

Why are costs important?

What are fixed costs?

What are variable costs?

Why is an economy of scale good?

Why is a dis-economy of scale bad?

Notes:

Before you listen

Discuss the following with your partner.

Price is not only the cost of something. Every purchase has a hidden cost. What do you think this is?

В F Listening

You're going to hear about another kind of cost called opportunity cost.Listen and choose the best answer for each question.Then listen again and check your answers.

What is opportunity cost?

A Something you have to give up in order to

have something else. В Something a company can charge people for